One of the keys in building wealth is having a solid foundation in budgeting.

Budgeting is your personal system on how you spend your money.

This article will discuss ways on how you can budget the easy way!

The Foundation of Budgeting

Every time you receive money, what comes into your mind?

You think of ways on how to spend that money, don’t you?

Such as what are the latest fashion items that you can buy or the latest destination to travel!

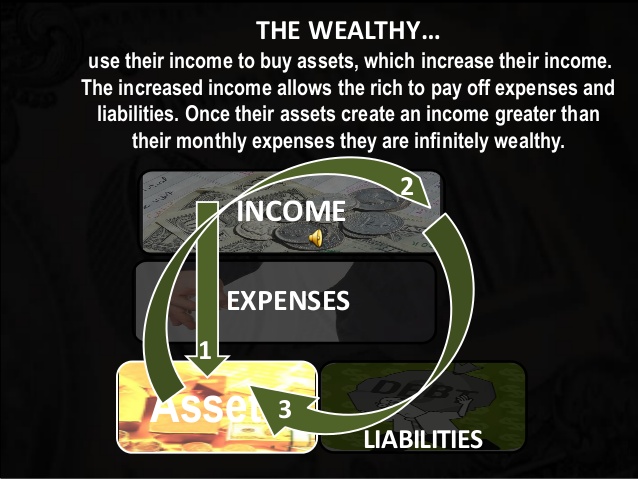

This is what we normally do:

INCOME – EXPENSES = SAVINGS

You receive your money, you spend it, and whatever is left (if there is any) is saved.

The foundation of budgeting in building wealth is this:

INCOME – SAVINGS = EXPENSES

You receive your money, you save a portion of it, and then spend whatever is left. Hence, you make sure that every time you earn money, you save a portion of it.

70-20-10 Rule

The problem with the formula EARNINGS – SAVINGS = EXPENSES is that it doesn’t tell you how much should be saved and spent.

The 70-20-10 Rules says that:

- 70% of your income should be spent of your living expenses

- 20% should be saved and invested, and

- 10% is allotted for charity, tithes, or what I call the giving fund.

Money Jar System

The 70-20-10 Rule gives us a good percentage on how we spend and save but does not really give a breakdown how we should spend our expenses.

My favorite budgeting system and what I use now is what I learned from T. Harv Eker’s The Millionaire Mind Intensive Seminar.

According to T. Harv Eker, you can use jars in budgeting called the Money Jar System.

You would be needing 6 Jars and label them as follow:

- Financial Freedom Account

- Long Term Saving for Spending

- Education Fund

- Play Fund

- Giving Fund

- Necessity/Living Expenses Fund

Financial Freedom Account ( FFA – 10%)

Allot 10% of your income to the Financial Freedom Fund. This is invested for the long term. Your goal here is to accumulate as much assets (stocks, rental properties, business, etc) as possible and live on it’s interest.

For example, if you would be needing P30,000 per month, multiply it by 12 months means your annual expenses in order to have a comfortable lifestyle is P360,000.

The goal is to be able to accumulate wealth that can give you P360,000 passive income every year.

Based on the example above, if you have a financial freedom fund of P3.6 Million, if it is invested in a financial instrument that earns 10% a year (P3,600,000 x 10%), it will give you P360,000 in interest which you can spend.

Or you can look for a rental property that can give you a rental income of P30,000 per month.

The goal here is not to stop working but to be financially free.

Meaning, you are already free not to work! You work because you choose to!

That for me is what I call FINANCIAL FREEDOM!

Long-Term Saving for Spending (LTSS – 10%)

Long-Term Saving for Spending are for big purchases such as a house, car, grand vacation. You save money and invest it in medium term low risk instruments in order to spend it in the near future.

Unlike the FFA wherein you don’t spend it, LTSS is basically there to be spent! It’s using your money to enjoy life and improve your standard of living.

Education Fund (10%)

Successful and wealthy people are avid learners. They read a lot of books every year sometimes ranging from 3-5 books a week. They continuously learn.

Remember this: No one became rich by being stupid.

The Education Fund is used to develop yourself and increase your value.

You can use it in order to buy books or attend seminars in order to increase your knowledge, skills, and network.

You can also use this to take further studies such as masters, doctorate, or have another degree you are passionate about.

Play Fund (10%)

Play Fund is what you use for your monthly or quarterly splurge.

This is for your Friday nights, movie nights, weekend getaways or fine dining splurges.

This will take away the guilt of spending your hard earned money.

We aim for a balanced life and by spending only 10% means you won’t blow up your budget during Pay Day Sales in malls or when you are down in life.

You can also save your Play Fund for “big splurges” but the maximum is 3 months. After saving for 3 months, you should spend it.

The reason being is that after not spending anything for 3 months, you will feel deprived and the probability of blowing up your budget and acquire debt will be very high.

To know more about this, read my article “3 Steps on How to Build Your Play Fund”.

Giving Fund (5-10%)

The giving fund is what you can use in giving to charity, church, or your loved ones.

This is where you get your budget when a family member ask for help or when you need to buy gifts for a party.

Gifts are usually expenses that we don’t budget. It results to spending more in a particular month especially if there are two birthday parties.

By having a Giving Fund, you make sure that you will be within your budget every month. Now, you can attend parties and not be embarrassed for not having a gift with you.

A Giving Fund helps you also to be generous especially for those who are in need.

Necessity/ Living Expenses Fund (50-55%)

The remaining is what you use for your living expenses: rent/mortgage, transportation/car payments, electricity and water bills, food and grocery, phone bills, etc.

In Summary, the Money Jar System is as follow:

- Financial Freedom Account – 10%

- Long Term Saving for Spending- 10%

- Education Fund- 10%

- Play Fund- 10%

- Giving Fund- 5-10%

- Necessity/Living Expenses Fund – 50-55%

Your Millennial Wealth Planner,

Harold Q. Gardon, CWP, CEPP

How do you find the article? Do you have any questions? Please feel free to message me if you want me to discuss a particular topic or if you are seeking financial advice.

How do you find the article? Do you have any questions? Please feel free to message me if you want me to discuss a particular topic or if you are seeking financial advice.

Subscribe to my mailing list and get a FREE copy of my e-book entitled “Millennial: A New Definition of Wealth”

We can also keep in touch through my FB Page.